Understanding Insurance Basics

Insurance is a financial mechanism designed to protect individuals and families against unforeseen risks and losses. At its core, insurance involves the transfer of risk from an individual or entity to an insurance company, which in turn provides financial reimbursement in the event of a loss. This process typically requires the policyholder to pay a premium, which is the amount charged for the coverage provided. Understanding insurance is crucial in ensuring that you have adequate protection against various life uncertainties.

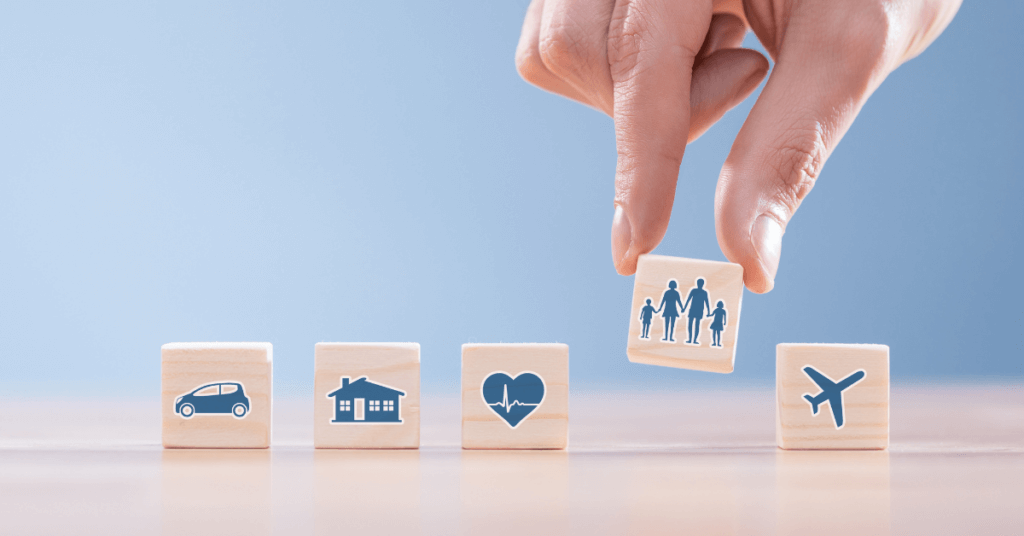

There are several types of insurance available, each serving a unique purpose. Health insurance is essential for covering medical expenses and can significantly alleviate the financial burden of unexpected healthcare needs. Homeowners’ insurance protects your dwelling and personal belongings against damage or theft, while auto insurance is mandated by law for car owners to cover liabilities resulting from accidents. Additionally, life insurance provides financial security for dependents in the event of the policyholder’s passing.

Key terms in the insurance realm include premiums, deductibles, and coverage limits. The premium is the periodic payment made to the insurance company to maintain your policy. This cost can vary based on factors like age, health, and the type of coverage chosen. The deductible represents the amount the policyholder must pay out-of-pocket before the insurance kicks in. Understanding this can help individuals make informed decisions regarding their financial responsibility in the event of a claim. Lastly, coverage limits denote the maximum amount an insurance policy will pay for a covered loss, highlighting the importance of selecting adequate coverage to suit one’s needs.

By familiarizing yourself with these foundational concepts of insurance, you will be better prepared to evaluate your options and secure the appropriate coverage necessary to safeguard your financial future.

Types of Insurance Available in the U.S.

The landscape of insurance in the United States is diverse, presenting individuals and families with a variety of options tailored to their specific needs. Understanding these different types of insurance can be essential for making informed decisions about protection and financial security.

Health insurance is one of the most critical forms of coverage, typically designed to help cover medical expenses. It plays a vital role in ensuring individuals have access to necessary healthcare services, from routine check-ups to emergency treatment. In the U.S., health insurance can be acquired through employer-sponsored plans, government programs like Medicare and Medicaid, or through private insurance companies. The Affordable Care Act has also expanded access to health coverage for many, emphasizing the importance of having health insurance to mitigate medical costs.

Another prevalent type of insurance is auto insurance, which is required by law in most states. This type of coverage protects policyholders against financial loss in the event of an accident, theft, or damage to their vehicle. It typically includes liability coverage, which pays for damages to other parties, as well as collision and comprehensive coverage for one’s own vehicle. Choosing the right auto insurance can significantly affect a driver’s financial situation in case of unforeseen events.

Homeowners insurance provides protection for individuals who own their property. This insurance covers damages to the home and its contents from various risks, including fire, theft, and certain natural disasters. It also offers liability coverage in case someone gets injured on the property. For renters, renters insurance serves a similar purpose, safeguarding personal belongings while providing liability protection. Lastly, life insurance is designed to offer financial security to dependents after the policyholder’s death, helping cover expenses like funeral costs or continuing living expenses.

Assessing Your Insurance Needs

Determining the appropriate insurance coverage is an essential step for individuals and families to safeguard their financial future. The process of assessing personal insurance needs requires careful consideration of various factors, such as family size, financial situation, health status, and property ownership. Each of these elements plays a crucial role in identifying the types and amounts of insurance necessary.

Family size is one of the first considerations when evaluating insurance requirements. Larger families may need more comprehensive health coverage, life insurance, and even disability insurance to ensure financial stability in the event of an unexpected incident. Additionally, those with dependents, particularly children, should assess the adequacy of their life insurance policies to provide for their loved ones in case of untimely death.

Your financial situation also significantly influences your insurance needs. Individuals with substantial assets may require higher levels of property insurance to protect against potential losses, while those with limited resources might focus on essential coverages to avoid overwhelming premiums. Furthermore, a clear understanding of your income, debt commitments, and savings can help you prioritize necessary insurance products without stretching your budget.

Health status is another critical factor to take into account. If you or your family members have pre-existing conditions or are at an increased risk of serious health issues, it may be wise to invest in more comprehensive health insurance policies. This ensures access to necessary medical care without substantial out-of-pocket costs. Lastly, property ownership, whether it involves a home, vehicle, or other valuable possessions, necessitates appropriate coverage to protect these assets against unforeseen events.

By taking these key considerations into account, individuals and families can develop a tailored insurance plan that adequately addresses their unique circumstances and provides peace of mind.

Researching Insurance Providers

When it comes to selecting an insurance provider in the United States, thorough research is vital to ensure you choose a company that aligns with your needs and expectations. Start by gathering a list of potential insurance providers that offer the specific type of coverage you require, whether it be health, auto, home, or life insurance.

One of the first steps is to check provider ratings. Organizations such as A.M. Best, J.D. Power, and the National Association of Insurance Commissioners (NAIC) offer detailed reports and ratings on various insurers. These ratings typically assess financial strength, customer satisfaction, and claims handling. This information can help you discern which providers have a good reputation for reliability and service.

Comparing premiums is another essential aspect of your research. While lower premiums can be attractive, they should not be your only consideration. Review the policy details and what is included in the coverage. Often, policies with lower premiums may offer reduced coverage or higher deductibles, potentially leading to higher costs in the event of a claim.

Customer reviews also provide insight into the experience other policyholders have had with a particular provider. Websites like Consumer Reports and Trustpilot allow individuals to share their experiences, both positive and negative. It is important to consider the overall trends in reviews rather than focusing on a few isolated opinions, as this can paint a clearer picture of the company’s customer service and claim settlement process.

Lastly, seek recommendations from friends, family, or financial advisors. Personal advice can often lead to discovering reputable insurance providers that have a proven track record. By employing a comprehensive approach that combines ratings, premium comparisons, customer reviews, and personal recommendations, you will be better equipped to make informed decisions regarding your insurance needs.

Getting Quotes and Comparing Policies

Obtaining insurance quotes is a crucial first step for consumers looking to secure the best coverage possible. The process begins by identifying various insurance providers, which can typically be accomplished through online research, referrals, or local agents. Many providers now offer easy-to-navigate online platforms where potential clients can input their information to receive personalized quotes. It is advisable to gather quotes from at least three different insurers to establish a comprehensive understanding of the market conditions.

When comparing insurance policies, it is essential to consider various factors beyond the initial premium. Coverage options should be analyzed carefully; a lower premium might accompany reduced coverage or higher deductibles. Understanding the specifics of these policies allows consumers to determine which option provides adequate protection relative to its cost. Additionally, evaluate the benefits included in each policy, as comprehensive coverage might save more money in the long run compared to minimal policies with lower upfront costs.

Deductibles represent another critical area to examine. A higher deductible often leads to a lower premium, but this trade-off could pose financial challenges in the event of a claim. Therefore, it is vital to assess your financial capacity to meet deductibles should a loss occur. Take time to read the fine print in policy documents; exclusions and limitations can significantly affect how well a policy meets individual needs.

Lastly, consider the financial strength and customer service reputation of the insurers you are evaluating. Ratings from independent agencies can provide insight into the reliability of an insurer during claims handling. By meticulously comparing quotes, coverage options, deductibles, and company reputations, consumers can make informed decisions and ultimately find insurance policies that best suit their needs and budgets.

Understanding Policy Terms and Conditions

When acquiring insurance, it is crucial for policyholders to possess a clear comprehension of the terms and conditions laid out within their insurance agreements. These documents, which may appear complex and lengthy, encapsulate essential information that dictates the coverage provided by the policy. A detailed review can prevent unexpected financial burdens in the face of a claim. Key components to scrutinize include exclusions, waiting periods, and renewal terms.

Exclusions are specific situations or conditions that the insurance policy does not cover. Understanding these limitations is vital as they inform the insured about potential scenarios where coverage is not applicable. For instance, many health insurance policies exclude certain pre-existing conditions or may not cover specific treatments. By identifying these areas, policyholders can make informed decisions or seek additional coverage if necessary.

Another critical aspect of policy terms is the waiting period. This is the duration an insured must wait before they can benefit from specific coverage. Common in health and life insurance, these waiting periods can significantly affect a policyholder’s access to timely care or benefits. Understanding when coverage begins is crucial, especially in situations requiring immediate attention.

Finally, renewal terms outline the conditions under which a policy can be renewed or modified upon expiration. Some policies automatically renew, while others may require active re-application. It is important for policyholders to be aware of any changes in premiums or coverage limits upon renewal. This knowledge allows individuals to plan their finances accordingly and avoid any lapse in coverage.

In summary, grasping the fine details of insurance policy terms, including exclusions, waiting periods, and renewal terms, is imperative for anyone seeking to navigate the complexities of insurance effectively. Being well-informed ensures that individuals can safeguard their interests and make choices conducive to their specific needs when obtaining insurance in the United States.

The Application Process

Navigating the insurance application process in the United States can be intricate yet manageable with the right guidance. The initial step involves determining the type of insurance needed—be it health, auto, life, or home insurance. Each category has its own requirements and intricacies, so understanding these distinctions is paramount.

Once the appropriate insurance type is identified, the next step involves gathering essential documentation. Typically, applicants will need proof of identity, such as a driver’s license or Social Security number, along with financial records that may include income statements, previous insurance policies, or credit reports. If applying for health insurance, medical history and current medications may also be necessary. Having these documents ready can streamline the application process considerably.

As you embark on the application, you will face a series of standard questions. Common queries often include personal information, desired coverage amounts, and details regarding any existing liabilities. Insurers may also inquire about your employment status and lifestyle habits, such as smoking or exercise routines, which can impact coverage options and premiums. It is crucial to provide accurate and truthful information, as any discrepancies can lead to complications during the underwriting phase.

The underwriting process is where the insurance company assesses your application and documentation. During this stage, underwriters analyze your risk profile based on the information provided. Expect some communication with the insurer for clarification or additional information. The duration of this process varies, but typically applicants can anticipate a waiting period of several days to weeks, depending on the complexity of the application.

As you move through these steps, it is advisable to keep open lines of communication with your insurance agent or representative. They can provide assistance, mitigate misunderstandings, and guide you through the nuances of policies offered. With proper preparation and understanding of the steps involved, you can successfully navigate the application process and secure the insurance coverage you need.

Strategies for Reducing Insurance Premiums

Lowering insurance premiums is a goal many policyholders strive for, as it allows individuals and families to save money while still maintaining adequate coverage. One of the most effective strategies to achieve this is by bundling insurance policies. Many insurance companies offer discounts for customers who choose to combine multiple policies, such as auto, home, and life insurance. This approach not only streamlines payment processes but can lead to significant savings on overall premiums.

Another practical method for decreasing insurance costs is to consider increasing deductibles. A higher deductible means that the policyholder agrees to pay more out-of-pocket in the event of a claim, which can result in lower premium rates. However, it is crucial for individuals to ensure that they can comfortably afford the higher deductible before selecting this option. Balancing the deductible with the total premium is essential to maintaining financial stability while securing affordable coverage.

Maintaining a good credit score is also instrumental in reducing insurance premiums. Insurers often use credit scores as a factor in determining risk, which can influence how much premium a policyholder will pay. By regularly checking credit reports for errors, paying bills on time, and managing debt effectively, individuals can improve their credit scores, which may consequently lower their insurance costs.

Lastly, taking advantage of various discounts offered by insurance companies can yield substantial savings. Many insurers provide discounts for good driving records, safety features in vehicles, and even for completing specific educational programs related to safe driving. Additionally, policyholders should inquire about other available discounts, such as those for being a member of certain professional organizations or alumni associations. Collectively, these strategies serve as valuable tools for lowering insurance premiums without compromising on essential coverage.

What to Do After Purchasing Insurance

Upon successfully purchasing an insurance policy, it is critical to take several proactive steps to ensure adequate understanding and management of your coverage. Firstly, reviewing and comprehending the policy documents is essential. These documents outline the terms and conditions, including coverage limits, deductibles, and the process for filing claims. Familiarizing yourself with these details not only helps in confirming that the policy aligns with your expectations but also empowers you to make informed decisions when utilizing your insurance.

Secondly, conducting regular policy check-ups is important for maintaining optimal insurance coverage. Situations often change, be it through life events such as marriage, home purchase, or the acquisition of valuable assets. Regular reviews allow you to assess whether your current policy still meets your needs or if adjustments are necessary. It is advisable to schedule these reviews annually or whenever a significant life change occurs. This practice ensures that all pertinent risks are adequately covered and that you are not underinsured or overpaying.

In the event that you need to file a claim, understanding the claims process outlined in your policy is vital. Immediately report any incidents to your insurer, providing all necessary documentation such as photographs, police reports, or receipts if applicable. Promptly initiating the claims process can facilitate a quicker resolution. Additionally, maintain an organized record of all communications and documents related to the claim, as this may prove invaluable should disputes arise during the process.

In conclusion, taking these steps after purchasing insurance not only secures your investment but also enhances your ability to navigate any future issues effectively, ensuring you remain well-informed and protected throughout your policy’s life cycle.