Home Insurance for a Senior: As a senior, ensuring your home is protected with the right insurance is essential. Whether you’re downsizing, living in a retirement community, or staying in your long-time home, home insurance provides financial protection against unexpected events such as fires, theft, or weather-related damage. However, obtaining verified home insurance as a senior can seem challenging due to factors like age, health status, and unique living situations.

In this guide, we’ll walk you through the steps to obtain reliable home insurance for seniors, offering tips to help you find the best coverage options at an affordable price. We’ll also provide a list of frequently asked questions (FAQs) to ensure that you have all the information you need when shopping for home insurance.

Why Do Seniors Need Home Insurance?

Home insurance is crucial for seniors to safeguard their property and belongings from unexpected events. As a senior homeowner, having the right coverage can also provide peace of mind, knowing that you won’t face financial hardship if something goes wrong. Here are a few reasons why home insurance is important for seniors:

- Protection Against Property Damage: Homeowners are vulnerable to unexpected events like fires, floods, or storms. Home insurance ensures that the cost of repairing or replacing damaged property is covered.

- Liability Coverage: Seniors often entertain guests or have visitors. Liability coverage protects against accidents or injuries that might occur on their property.

- Peace of Mind: Seniors may have lived in their homes for many years and accumulated valuable possessions. Insurance helps protect these assets, which may be irreplaceable.

- Financial Security: With rising medical costs and fixed incomes, seniors may struggle to cover large expenses. Insurance can help reduce the financial burden if damages or accidents occur.

Steps to Obtain Verified Home Insurance for Seniors

1. Understand Your Coverage Needs

Before you start shopping for home insurance, it’s important to understand the types of coverage you need. Different homeowners may have different needs based on their living situation, possessions, and budget.

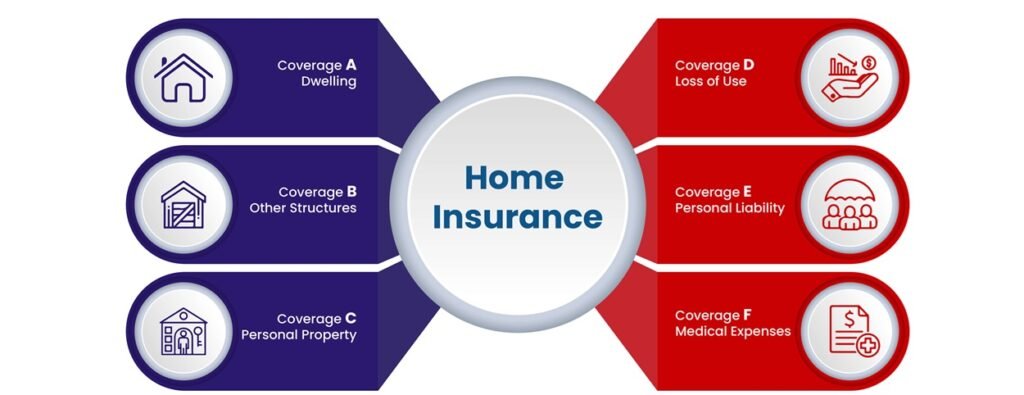

Key types of coverage to consider:

- Dwelling Coverage: Protects the structure of your home against damage from fire, storms, or other covered events.

- Personal Property Coverage: Covers the cost of replacing your belongings in case of theft, fire, or other damage.

- Liability Coverage: Protects you from financial loss if someone is injured on your property.

- Loss of Use Coverage: Covers living expenses if your home becomes uninhabitable due to damage.

As a senior, your needs may be different from younger homeowners. For example, if you live in a retirement community or a mobile home, you may need a specific type of policy that fits your living situation.

2. Research Insurance Providers Specializing in Senior Homeowners

Not all home insurance providers offer the same level of coverage or pricing for seniors. Some companies may have policies tailored specifically for older adults, with coverage options that meet the unique needs of senior homeowners. These providers often consider factors like age, home condition, and health when calculating premiums.

To start, research reputable insurance companies that have a good track record of serving senior citizens. Look for:

- Companies with strong customer service and positive reviews.

- Providers that specialize in affordable coverage for seniors.

- Insurers that offer discounts for seniors, such as loyalty discounts or multi-policy discounts.

3. Compare Multiple Quotes

One of the best ways to ensure you’re getting a verified and affordable home insurance policy is to compare quotes from multiple insurance providers. Online comparison tools make this process simple and allow you to find the best deals based on your home and financial situation.

When comparing quotes, consider:

- Premiums: The amount you pay monthly or annually for coverage.

- Deductibles: The amount you must pay out of pocket before your insurance kicks in.

- Policy Limits: The maximum amount your insurer will pay for a claim. Make sure the limits are sufficient to cover potential damages.

- Exclusions: Ensure you understand what is not covered by the policy, as some companies may exclude certain types of damage, such as flood or earthquake coverage.

Take the time to carefully evaluate each quote to ensure you are receiving verified and competitive offers from reputable insurance companies.

4. Look for Senior-Specific Discounts

Many insurance companies offer discounts for senior citizens, which can help lower your premiums. These discounts can vary depending on the insurer, but common options include:

- Age-based discounts: Some insurers offer reduced premiums for homeowners over the age of 55 or 60.

- Claims-free discounts: If you haven’t filed a claim in a certain number of years, you may qualify for a claims-free discount.

- Bundling policies: If you have other insurance policies, such as car or life insurance, you may be eligible for a bundling discount.

- Safety and security discounts: If you have certain home safety features (such as smoke alarms, fire extinguishers, or security systems), you may receive a discount on your home insurance policy.

Be sure to ask about these discounts when you’re speaking with insurance agents or requesting quotes. The more discounts you can qualify for, the more affordable your premiums will be.

5. Review the Insurance Policy’s Fine Print

Before finalizing your decision, always read the fine print of your insurance policy. This will help you understand the terms, coverage limits, and exclusions that may affect your ability to file a claim in the future.

Pay attention to:

- Exclusions: Common exclusions in home insurance policies include damage from floods, earthquakes, or routine wear and tear. If your area is prone to natural disasters like floods or earthquakes, you may need additional coverage for these events.

- Claims process: Review the process for filing claims and the timeframe for receiving compensation. Make sure you’re comfortable with the insurer’s claims process.

- Payment options: Verify whether the insurer offers flexible payment plans that work with your budget. Some companies allow you to pay monthly or quarterly.

6. Consider the Insurer’s Reputation

The best home insurance companies for seniors are those that have a reputation for excellent customer service, fair claims processes, and reliable coverage. Look for insurers that have:

- A strong financial rating: Check ratings from organizations like A.M. Best or Standard & Poor’s to ensure the insurer is financially stable and able to pay claims.

- Positive customer reviews: Look for feedback from other senior homeowners regarding their experiences with the insurer. Customer satisfaction is a key indicator of how well an insurer will handle your policy.

7. Consult an Independent Agent

If you’re feeling overwhelmed by the choices available, consider consulting an independent insurance agent. Independent agents work with multiple insurers and can help you navigate the process of finding the best home insurance for seniors. They’ll take the time to understand your specific needs and help you compare policies to ensure you get the best deal.

FAQs About Home Insurance for Seniors

1. Do seniors pay higher premiums for home insurance?

In general, seniors may pay slightly higher premiums for home insurance, especially if they are older or have health conditions that could make them more vulnerable to accidents. However, many insurers offer discounts for seniors, which can help lower the cost of coverage.

2. Can a senior get home insurance if they don’t own their home?

Yes, seniors who rent or live in an apartment can still obtain renters insurance, which provides coverage for personal property and liability. Renters insurance is often more affordable than homeowners insurance, but it’s just as important to protect your belongings.

3. Are there any insurance providers that specialize in senior homeowners?

Yes, some insurers specialize in serving senior homeowners. They may offer specific coverage options, pricing, and discounts tailored to seniors’ needs. It’s important to research these providers to find the best policy for your situation.

4. What is the best way to lower home insurance premiums for seniors?

To lower premiums, seniors can take advantage of discounts, such as bundling policies, installing safety features in the home, or maintaining a claims-free record. Shopping around and comparing quotes is also a great way to find the most affordable options.

5. Is flood insurance necessary for seniors?

If you live in a flood-prone area, you may want to consider adding flood insurance to your home insurance policy. Standard home insurance policies typically do not cover flood damage, so it’s important to purchase separate flood insurance if needed.

6. Can I get home insurance if I have a pre-existing medical condition?

Yes, home insurance is not based on your medical condition. However, some insurers may consider factors like your home’s safety features and your ability to maintain the property when determining rates.

Obtaining verified home insurance for seniors is essential to protecting your home, belongings, and finances. By following the steps outlined above, you can secure the right coverage at a price you can afford. Take the time to compare different providers, review your policy options, and ask about available discounts to ensure you get the best deal on your home insurance policy.