From understanding health insurance terminology like “deductibles” and “copays” to deciphering the contents of a bill, consumers can face various barriers when trying to understand the costs associated with their health insurance coverage. This lack of understanding may contribute to frustration and cost-related problems and can have far-reaching effects on consumer health and finances. The KFF 2023 Survey of Consumer Experiences with Health Insurance (“KFF Consumer Survey”) found that 27% of insured adults reported that their health insurance paid less than they expected for a bill they received from a doctor, hospital, or lab in the past twelve months, the biggest cost-related problem consumers reported experiencing. Efforts to make cost information more readily available and easy to understand could help reduce some of these problems.

The first brief of this two-part series on navigating health insurance complexities and consumer protections focused on how consumers understand what their health insurance covers, what they do when coverage is denied, and what federal protections exist to ensure that the information available to them and coverage determinations are fair, accurate, and timely. This second brief focuses on KFF Consumer Survey findings about consumers’ understanding of health insurance costs and examines existing federal protections that seek to address barriers to understanding the cost of coverage and care, such as price transparency, self-service price estimator tools, and simplifying cost-sharing designs.

KFF Consumer Survey Findings: Consumer Understanding of Costs Associated With Health Coverage

The KFF Consumer Survey included a nationally representative sample of 3,605 U.S. adults ages 18 and older with health insurance. The survey asked consumers how well they understand costs associated with their health coverage, cost-related health insurance terminology, and the difficulty level of comparing cost-related insurance options such as premiums and deductibles.

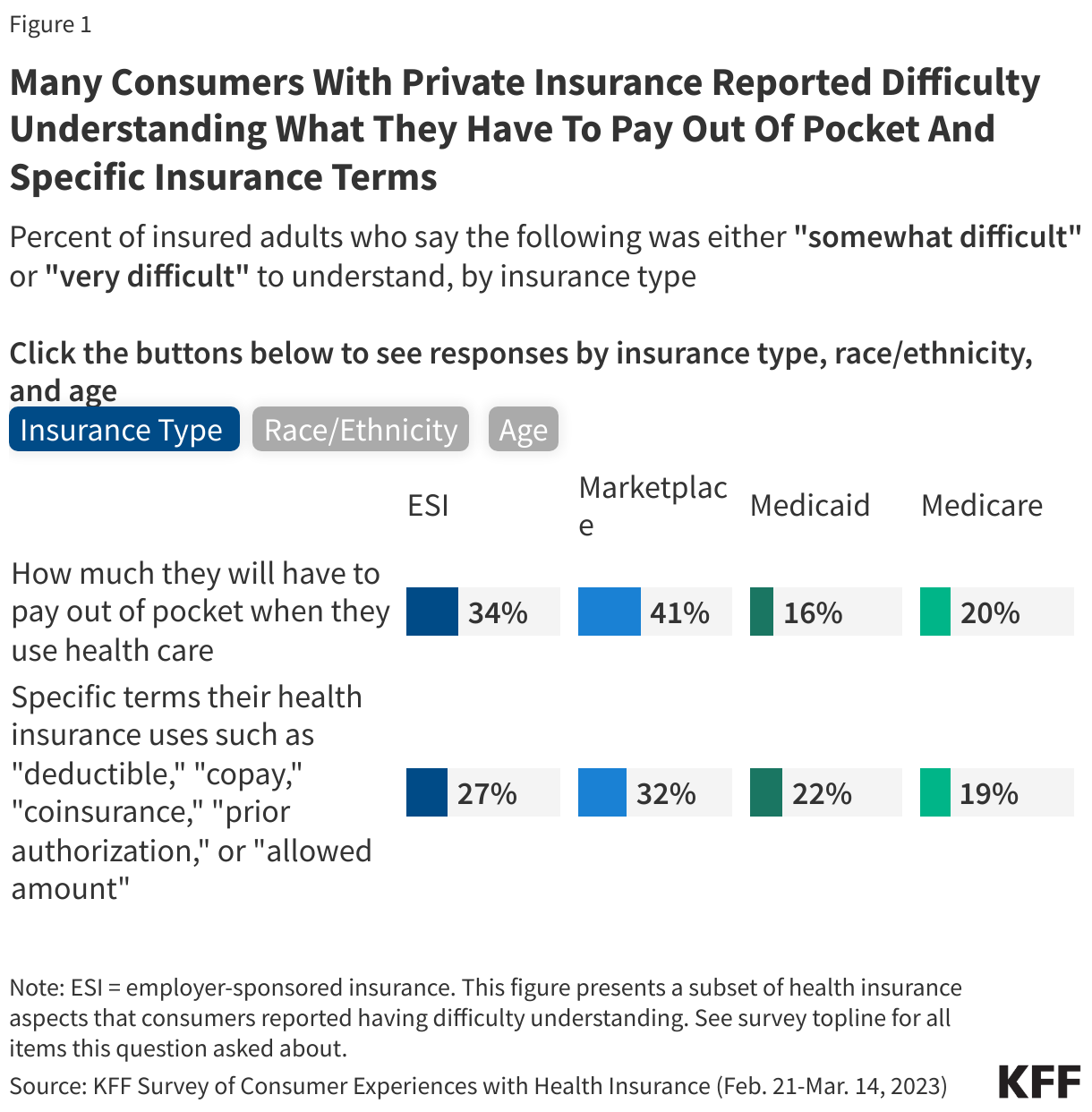

Three out of ten adults (30%) said that it was somewhat or very difficult to understand how much they would have to pay out-of-pocket when they use their health insurance. Marketplace (41%) and ESI (34%) enrollees were more likely to report this difficulty compared to Medicaid (16%) and Medicare (20%) enrollees (Figure 1). Insured White (30%) and Hispanic (32%) adults were more likely to report that it was somewhat or very difficult to understand how much they will have to pay out of pocket when they use health insurance compared to Black adults (23%). Additionally, insured adults ages 18-29 (35%), 30-49 (35%) and 50-64 (30%) were all more likely to report that it was somewhat or very difficult to know how much they will have to pay out of pocket when they use health insurance compared to those ages 65 and older (18%).

One-quarter (25%) of insured adults said that it was somewhat or very difficult to understand specific terms that their health insurance uses such as “deductible,” “copay,” “coinsurance,” “prior authorization,” or “allowed amount.” Those with Marketplace coverage (32%) and ESI (27%) were more likely to report that it was somewhat or very difficult to understand these terms compared to those with Medicaid (22%) and Medicare (19%) (Figure 1). Furthermore, Hispanic adults (31%) were also more likely to report difficulty in understanding these terms compared to White (23%) or Black (22%) adults. Insured adults between the ages of 18-29 (29%), 30-49 (30%), and 50-64 (25%) were all more likely to report difficulty in understanding these insurance terms compared to those ages 65 and older (17%).

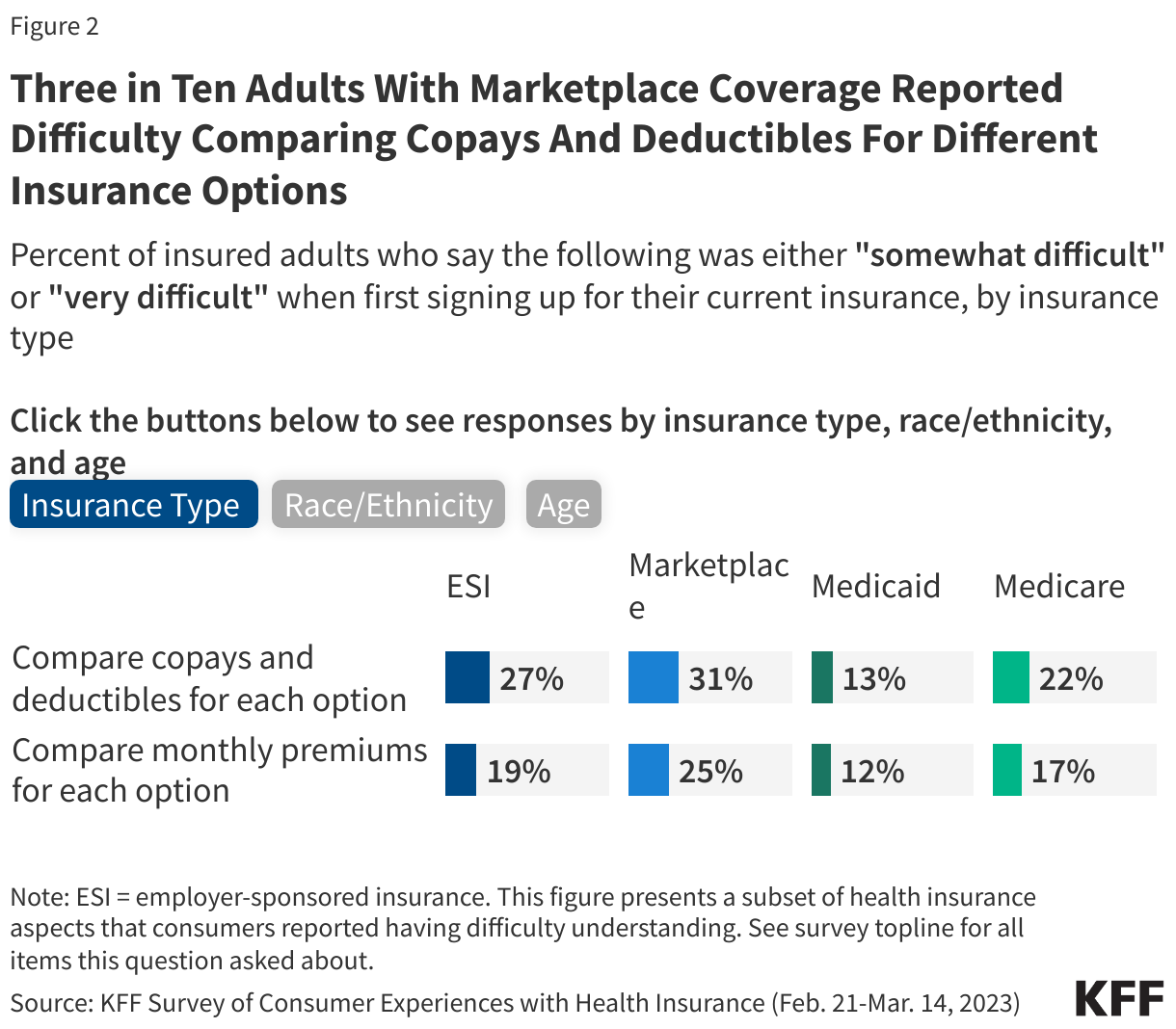

One in four (25%) insured adults reported that it was somewhat or very difficult to compare the copays and deductibles for each plan option. Those with ESI (27%) and Marketplace (31%) coverage were more likely to report having this problem compared to those with Medicaid (13%) or Medicare (22%) (Figure 2). A larger share of insured White (24%) and Hispanic (27%) adults reported difficulty comparing the copays and deductibles for each option than Black (19%) adults. Additionally, insured adults ages 18-29 (28%) and those ages 30-49 (27%) were more likely to report that it was somewhat or very difficult to compare the copays and deductibles for each option compared to those ages 65 and older (21%).

About one in five (19%) insured adults reported that it was somewhat or very difficult to compare the monthly premiums for each coverage option. Those with Marketplace coverage (25%) were more likely to report having this issue compared to those with ESI (19%), Medicaid (12%), or Medicare (17%) (Figure 2). Insured Hispanic adults (22%) were more likely to report difficulty comparing the plan premiums than White (17%) adults. Insured adults ages 18-29 (24%), 30-49 (20%), and 50-64 (19%) were all more likely to report that it was somewhat or very difficult to compare the monthly premium for each option compared to those ages 65 and older (13%).

Federal Consumer Protections that Seek to Address Barriers to Understanding the Cost of Coverage and Care

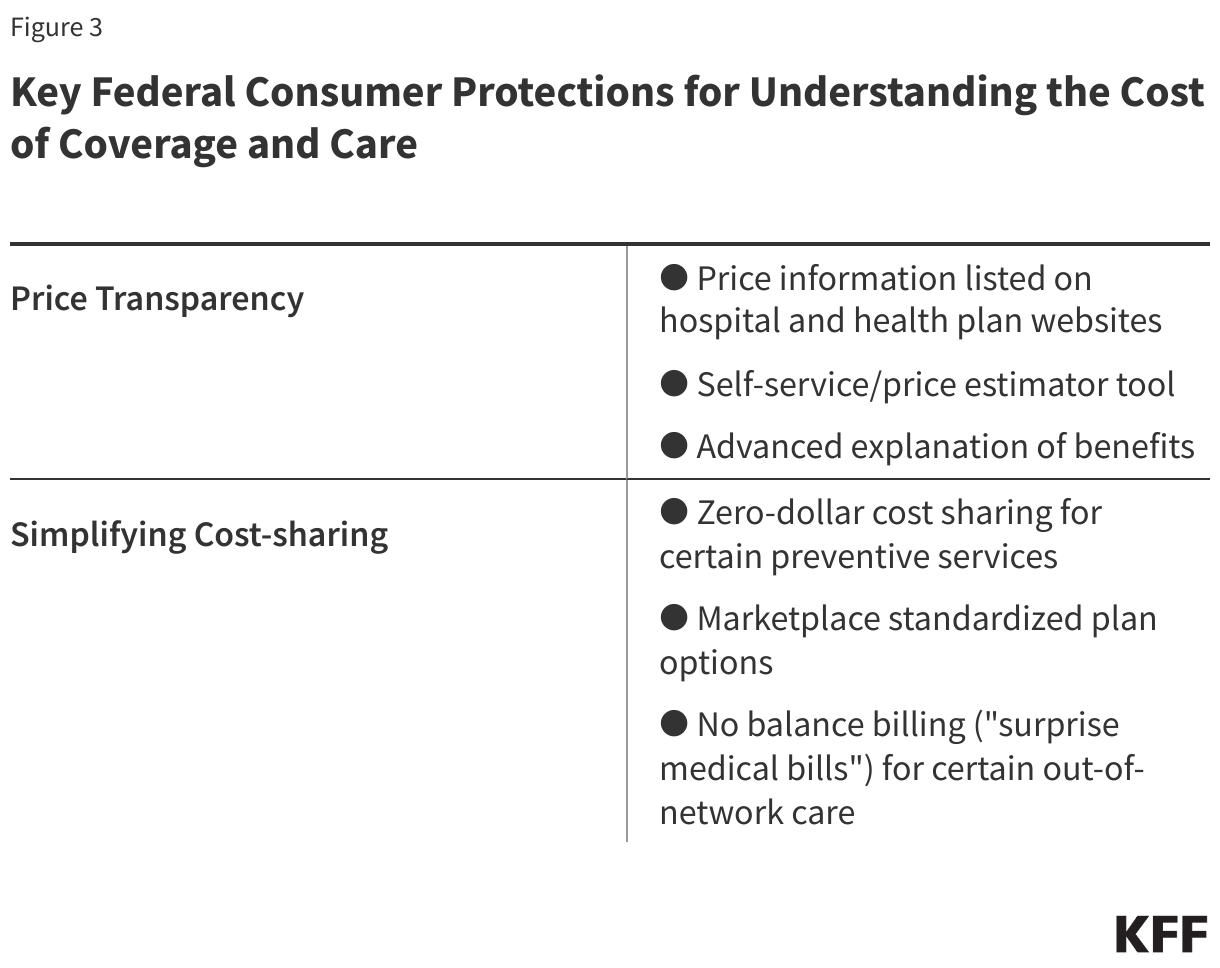

The KFF Consumer Survey indicates that many consumers have gaps in understanding what they will have to pay for the services they need before they receive care. Federal reforms related to health insurance costs aim to simplify and standardize cost sharing, set guidelines for the coverage of certain health benefits, and promote price transparency. Some of these changes may enable consumers with private coverage to better understand their coverage options and out-of-pocket obligations for covered benefits. This section focuses primarily on federal protections for individuals with private health insurance (individual and employer-sponsored), though public programs like Medicare and Medicaid have established many consumer protections as well.

Providing Consumers with Cost Specific Information: Price Transparency

Federal reforms to private insurance aim to increase price transparency and promote competition among hospitals and among insurers, reduce health care costs, encourage patients to price-shop at different facilities by providing an estimate of patient out-of-pocket costs for a health care service or prescription drug, and help consumers make better plan selections. Reforms would allow consumers to look for price information about a service in at least three ways:

Search listed pricing information available on hospital and plan websites: Most hospitals in the U.S. are required to establish, update annually, and make public on the internet a comprehensive machine-readable file containing a list of their “standard charges” for all items and services that they provide. Standard charges are the regular rates established by hospitals for items and services. Standard charges alone are generally of less value to insured consumers when determining their out-of-pocket costs than the “allowed amount,” which is the maximum amount a specific health plan will pay for a covered benefit. This hospital price transparency requirement was included in the Affordable Care Act (ACA), with more extensive federal regulations (incorporating additional forms of pricing, including allowed amounts) issued in 2019 and effective in 2021. Separate federal price transparency standards require employer-sponsored plans and insurers to post on a publicly accessible internet site three machine-readable files disclosing different forms of pricing information specific to each plan: in-network provider-negotiated rates, historical out-of-network allowed amounts (the maximum amount a plan will pay for a covered health service received from an out-of-network provider), and prescription drug rates. Health plans and insurers must update these machine-readable files at least monthly and clearly state when it was last updated. This “Transparency in Coverage” requirement was created by 2020 regulations interpreting a provision in the ACA related to consumer transparency. These postings have been required since 2022, although full implementation of the prescription drug reporting was delayed.

The information posted to date under these two requirements is anything but consumer-friendly, as experts have noted their own problems evaluating the data. Data scientists and other researchers have reported finding this information overwhelming and sometimes inaccurate and difficult to decipher. As third-party entities aggregate this data to assist employer plans to make purchasing decisions and public policy researchers to evaluate costs, consumers themselves likely have limited ability to use the raw data on their own. There are few studies of the consumer experience with this machine-readable data, especially whether they know it is available, and their ability to understand and use it.

Use a self-service or price estimator tool: In an effort to alleviate the complexity and possible confusion that was perhaps anticipated by policymakers when requiring the posting of large amounts of data in digital files, federal rules also require that more “consumer-friendly” tools be available so that consumers can obtain information about out-of-pocket costs before they get a service or drug. Under the hospital transparency regulation, hospitals must also compile and display online a “consumer-friendly” list of at least 300 “shoppable” services (e.g., having a baby, getting a hip replacement), including 70 services specified by the Centers for Medicare & Medicaid Services (CMS) and any additional procedures chosen by the hospital. The list must include a plain language description of each procedure, discounted cash prices, payer-specific (i.e., private insurers, Medicare, Medicaid) negotiated prices, and de-identified minimum and maximum negotiated prices for all third-party payers for an item or service. As an alternative to this “consumer-friendly” list, a hospital can instead create and maintain an online price estimator tool that:

- Provides estimates for at least 300 shoppable services (including the 70 CMS-required services).

- Is displayed on the hospital website for easy access (i.e., does not require payment or the creation of an account to use the estimator tool); and

- Allows consumers to obtain an estimate of the amount they will be expected to pay the hospital for the shoppable service before they receive it.

The Transparency in Coverage regulation requires plans and insurers to provide cost-sharing information via an internet self-service tool that consumers can use to obtain personalized out-of-pocket estimates for in- and out-of-network health care items and services (including prescription drugs and medical equipment). Plans and insurers must make other information—such as the negotiated rate for a service, and whether the service is subject to prior authorization—available through a billing code or service description search. This rule was fully effective in 2024.

In addition, in 2020 Congress passed and President Trump signed the Consolidated Appropriations Act (CAA), which required plans and insurers to make a “price comparison tool” available on the internet, in paper form, and by telephone. Since this tool is similar to the Transparency in Coverage self-service tool, federal agencies state in guidance that they have deferred enforcement of this CAA price comparison tool requirement.

Review an Explanation of Benefits before care is received (Advanced Explanation of Benefits (AEOB)): In addition to the transparency initiatives above, Congress also included in the CAA another transparency-related protection—the Advanced Explanation of Benefits—to help consumers better understand their expected out-of-pocket cost for a service before they receive it so they can budget and/or compare cost to other providers. This was part of the No Surprises Act, a group of consumer protections included as part of the CAA.

When scheduling care or upon request health care providers and facilities must provide a personalized good faith estimate of the provider’s expected charges to the consumer’s employer plan or insurer. The plan or insurer must then use this information to create an Advanced Explanation of Benefits for the consumer that includes standard Explanation of Benefits information such as the provider’s expected charge, what the plan expects to pay, and the amount the consumer is expected to pay.

Implementation of this provision of the law has been challenging, according to CMS, as it will require coordination between providers and plans, and likely the development and testing of a single industry-wide electronic interchange standard. The agencies involved had convened an industry working group as well as consumer testing with prototype Advanced Explanation of Benefits. The rule’s 2022 effective date has been delayed.

Although the Advanced Explanation of Benefits has not yet been implemented, providers and facilities must provide a good faith estimate to uninsured and self-pay patients upon request or in advance of a scheduled service, within a specified timeframe. If the final bill is $400 or more above the good faith estimate, consumers may be able to dispute the bill through a patient-provider dispute resolution process. Eligible consumers may submit a complaint to CMS if the provider did not give the patient a good faith estimate or if the provider does not honor a dispute resolution in the patient’s favor.

Simplifying Cost Sharing and Other Consumer Out-of-Pocket Payments to Limit Cost and Address Complexity

The ACA ushered in new federal requirements to limit out-of-pocket spending for consumers with private insurance, with protections that set parameters for the design of certain health plan options and limited cost sharing so that it is the same whether the consumer has employer coverage or other private coverage on- or off- Marketplace. Marketplace plans have gone further through standardized plan options. The No Surprises Act’s reforms address balanced billing, eliminating it for certain services. All look to make costs more understandable and predictable for patients. These protections include:

Maximum out-of-pocket limit: All non-grandfathered private plans are required to set an annual cap on cost sharing for essential health benefits received in-network. These dollar limits are adjusted each year. For the 2025 plan year, the maximum out-of-pocket limit is $9,200 for self-only coverage and $18,400 for family coverage. Once a consumer reaches the maximum out-of-pocket limit, the insurer is required to cover 100% of the cost of essential health benefit services received in-network for the remainder of the plan year.

Ban on annual and lifetime dollar limits: All private plans, including grandfathered plans, are prohibited from imposing annual or lifetime dollar limits on coverage for essential health benefits, whether for in-network or out-of-network services. An annual dollar limit refers to the maximum amount an insurer would pay for covered benefits within a given year, whereas a lifetime dollar limit is the total dollar amount that a health plan would pay for as long as a consumer was enrolled in the plan. Prior to the passage of the ACA, an estimated 70 million people in large employer plans, 25 million in small employer plans, and 10 million with individual coverage had lifetime limits on their health coverage.

Zero-dollar cost sharing for certainpreventive services: Under the ACA, all private, non-grandfathered plans must cover a range of preventive services and not apply cost sharing, including:

- Evidence-based screenings and counseling for adults recommended by the U.S. Preventive Services Task Force (USPSTF) with an “A” or “B” rating such as cancer screenings, prenatal care, and medications that help prevent heart disease

- Routine immunizations for adults and children recommended by the Centers for Disease Control and Prevention’s Advisory Committee on Immunization Practices such as influenza, measles, and COVID-19

- Preventive care for infants, children, and adolescents recommended by Health Resources and Services Administration’s (HRSA) Bright Futures Program such as well-child visits, autism screening, and fluoride supplements

- Additional preventive services for women as recommended by HRSA’s Women’s Preventive Services Initiative such as contraception, breast cancer screening, and breastfeeding supplies and support

Marketplace standardized plan options: Plans in the Marketplace are separated into categories — Bronze, Silver, Gold, or Platinum — based on the amount of cost sharing they require. In general, plans with lower cost sharing have higher premiums, and vice versa. For example, Bronze plans have the highest cost sharing but lower premiums, and Platinum plans have the lowest cost sharing but higher premiums. There can be substantial variation in plan details, even within the same insurer (e.g., premiums, provider networks, covered benefits, plan network types).

Standardized plan designs (also known as “easy pricing”) were created to simplify and streamline plan comparison and selection offered on the federally facilitated Marketplace (FFM), state-based exchanges using the federal platform (SBE-FPs), and some state-based Marketplaces (SBMs) by applying the same deductibles, copays, coinsurance, and out-of-pocket maximums to each category of essential health benefits across all Easy Price plans in the same metal level. For example, in 2025, the annual deductible for covered services under all Gold level Easy Price plans is $1,500, regardless of insurer. By contrast, other non-standardized Gold level plans might have different deductible and copay amounts.

Standardized plan design options were also designed to improve affordability by covering certain services before the deductible is met. All Easy Price plans must waive the deductible and instead apply a fixed dollar copay (e.g., $30 for a Gold Easy Price plan) for the following items and services: primary care and specialist office visits, urgent care visits, outpatient visits for mental health and substance use disorder treatment, physical therapy visits, and generic and preferred-brand drugs.

Not all Marketplace plans are standardized, though Marketplace plans must offer a standardized plan option at every product network type, metal level, and throughout each service area where they offer non-standardized plan options. Insurers can still choose to offer non-standardized plan options in the individual market but are limited to two plan options per product network type (i.e., HMO, PPO, EPO, POS) for plan year 2025.

Research has shown that having too many choices can confuse consumers and lead to them choosing suboptimal coverage. As implemented to date, HealthCare.gov’s requirement to offer standardized plan options may have increased, not decreased, the number of plan choices consumers face. Though consumers in most areas will continue to have a large number of plan choices for the foreseeable future, over time, that number may become more manageable.

Prohibition on balance billing for certain out-of-network care: Also known as “surprise medical bills,” balance billing can occur in medical emergencies, when insured patients are not necessarily able to choose an in-network hospital or provider as well as in non-emergencies when patients inadvertently receive care from an out-of-network provider at an in-network facility. In these cases, patients can be liable for the balance bill from the provider plus any cost sharing under their health plan. As of 2022, many of these types of balance bills are now prohibited under the No Surprises Act. The No Surprises Act generally protects patients with individual and employer-sponsored insurance by:

- Requiring private health plans to cover these out-of-network claims and apply in-network cost sharing for certain covered benefits.

- Prohibiting out-of-network providers, facilities, and providers of air ambulance services from billing patients more than in-network cost sharing for certain out-of-network care.

- Requiring providers and facilities to provide patients with written notice explaining surprise billing protections, who to contact for concerns about potential violations, and how they can waive billing protections if they choose to do so.

Looking Forward

Consumer understanding of their coverage costs can play a significant role in seeking needed health care. One study found that lower health literacy scores were associated with consumers delaying or forgoing preventive care due to perceived health care costs. While better consumer education and outreach can help, the inherently complicated and profit-driven insurance and health care system includes few incentives to provide consumers with individualized and impartial assistance. However, several existing consumer protections, if implemented and enforced, as well as a broader health policy focus on how to improve the consumer experience, could make a difference.

Focus on price transparency: Despite a deregulatory agenda and recent cuts to agency staff, the Trump administration has directed the agencies to better enforce price transparency regulations. However, these machine-readable files with lists of prices and procedure codes currently have limited value to help consumers directly without an impartial analysis of the data and user-friendly vehicles to describe the information. Price estimators, also required as part of the Transparency in Coverage rule, have the potential to have more value to patients. However, while consumers may want an estimate of their expected out-of-pocket costs for a covered benefit, their awareness of the existence of these estimator tools and the likelihood of using them will influence how effective the regulation is at achieving its aims. Research conducted before and after its implementation showed mixed results on the consumer experience using these tools and their effectiveness in lowering out-of-pocket costs and health care costs overall. There is also concern that consumers will conflate high-cost with high-value care when price estimator tools do not incorporate quality metrics, potentially leading to higher health care spending. In an era of rapid developments in digital technology and artificial intelligence, ways to improve, consumer test, and standardize these tools and encourage their use may be one area of future focus.

Spotlight on cost-sharing protections: Getting renewed attention in the coming months and years are standardized cost-sharing designs that have or have the potential to provide more transparency and predictability about out-of-pocket costs for consumers. The U.S. Supreme Court will decide a case that could end free coverage of certain preventive care services recommended by the U.S. Preventive Services Task Force. A decision in that case is expected later this year. Consumers also await implementation of the Advanced Explanation of Benefits, as a key tool for patients to get cost information upfront. The coordination between plans and providers required for this initiative could go a long way to help patients often caught in the middle between plans and providers not working with each other in the best interest of consumers.

Finally, look for more attention to prescription drug costs and a cost-sharing protection that has been in place across all private insurance for over a decade, the maximum out-of-pocket limit, or cost-sharing limit. Many people who take certain high-cost medications receive financial assistance from drug manufacturers to offset their out-of-pocket costs. In recent years, private plans (excluding those offered to federal workers) have increasingly applied copay accumulators and copay maximizers when an enrollee receives this manufacturer assistance. Under these types of adjustment programs, the amount of financial assistance an enrollee receives does not count toward an enrollee’s out-of-pocket obligations, including the maximum out-of-pocket limit. Research has found that there is little transparency in how these programs operate and research has demonstrated that consumers are not always aware that their health plan contains these features. After a court challenge and a recent change in essential health benefit regulations, the federal government might be poised to confirm and clarify that cost sharing includes amounts received from pharmacy financial assistance programs and that plans must count those amounts toward the maximum out-of-pocket limit.

Continuing state-level initiatives to improve cost transparency: State-level initiatives that aim to improve cost transparency and help prevent medical debt could play a larger role if federal enforcement and regulations concerning consumer protections are stalled. New York, for example, enacted a bill in 2024 that bans a common provider practice, requiring patients to agree to cover the costs of a bill that their insurer does not cover before services are rendered (referred to as a “consent-to-bill” form) and requiring providers have a discussion with their patients about costs of services before signing this form. Although the state has indefinitely delayed full implementation of this law, the requirement for providers to discuss costs with the patient before asking them to sign the consent-to-bill form would still apply.

States continue wide-ranging activity to address high prescription drug costs in private insurance as public concern about high prescription drug costs continues to mount. For example, pharmacy benefit manager (PBM) practices have been criticized for driving up prices and for being shrouded in secrecy. In response, many states have passed laws that aim to improve PBM transparency and reporting requirements, prohibit PBM policies that prevent pharmacists from telling patients when a lower-cost option might be available, and prohibit PBMs from steering enrollees to PBM-owned pharmacies, among others. Whether these laws apply to all private insurance, including self-insured private employer plans, is an open question.

This work was supported in part by a grant from the Robert Wood Johnson Foundation. The views and analysis contained here do not necessarily reflect the views of the Foundation. KFF maintains full editorial control over all of its policy analysis, polling, and journalism.